“Super Apps” are Coming; SQ & PYPL Highlights; BNPL Race is On

By Tito Donis

May 10, 2021

Greetings,

What an exciting week. Apps are gaining superpowers. Cryptos are powering to all-time highs. And the lines where fintech begins and ends is blurring.

This week, we look at key highlights from PayPal and Square’s Q1 Earnings and Klarna’s role in the BNPL race.

New here? Subscribe now to get our newsletter each Sunday.

Job Market Continues to Struggle; Stocks Continue to go Up

April jobs report showed only 266,000 jobs were added. Much lower than the 1 MM expected by economists.

Stocks rose on the news due to continued expectations of “money printer go brrrrrrr” conditions.

BNPL Race — Klarna Leading App Download Volumes

Klarna had over 4.4 MM app downloads in Q4 2020 for the U.S. segment, which is more than Affirm and Afterpay combined. Downloads were up 140% from Q3, most likely driven by holiday shoppers flocking online during lockdowns. It’s not clear how much marketing spend is behind the app store push.

Klarna’s downloads in Europe during Q4 were 7.6x greater than Clearpay, their second biggest competitor in the space.

In terms of spending, Klarna also outpaced Afterpay globally, recording $53 Bn in sales compared to Afterpay’s $11.1 Bn in 2020.

BNPL is one of the many asset classes on the PeerIQ platform.

If you would like to learn more, please reach out to sales@peeriq.com.

PayPal Building “SuperApp” — Focused on BNPL and Crypto

“Super Apps” are coming to the U.S. with PayPal and Square leading the charge.

Venmo and Cash App are looking to replace your physical wallets with digital wallets on your phone.

PayPal’s core idea is to build the one app to rule them all — a “superapp” that will provide customers with “customized shopping, financial services, and payments”

There are a few codewords here — let’s translate this sentence to: “PayPal will provide customers with integrated e-commerce, lending, payments, and payroll financing services.”.

That’s our best sense of where PayPal is quietly-not-so-quietly going. The lines that previously separated industry categories (e.g., FinTech lenders, trading, peer-to-peer payments, etc.) is blurring.

And it makes sense — customers want a unified experience that delivers value from a trusted institution. It may make sense for fintech lenders that historically have had a one-time transactional lending relationship to consider renting white-label tech to close the offering gap.

Here’s an excerpt from PayPal’s investor deck.

PayPal is also making a big push on crypto and BNPL. Both markets continue to grow briskly, but also plenty of new entrants are looking for their fare share.

It’s notable that every digital fintech firm is offering crypto trading (RobinHood, TastyTrade, SoFi, Square, etc.).

On BNPL, PayPal is growing quickly. The question here is how long can POS lenders maintain 30%+ growth rates across a sector where others (Affirm, GreenSky, AfterPay, and others) are competing for merchants?

Still, there’s plenty to do in BNPL in embedded finance solutions (WiseTack) and also financing for underserved categories. Lending to professionals (dentists, doctors, accountants, etc.), where there is less competition and it is easy to access and underwrite customers, still appears to be underserved.

Other PayPal Stats:

PayPal (PYPL): Market Cap: $297.5 Bn, P/E ratio 57.7x, P/S ratio: 12.8x

- Revenue of $6.0 Bn in Q1 2021 (+31% YoY); Free Cash Flow of $1.5 Bn (+27% YoY)

- PayPal is focused on extending Venmo’s commerce and crypto capabilities

- Announced Venmo “Super App’’ to rollout in Q3.

- Daily active users +33% in Q1 driven by Venmo customers who buy, sell, and hold cryptocurrency. “About half of our crypto users open their app every single day”

- “Cash is definitely being replaced…[every] country around the world in which we’ve engaged…[is] envisioning a future…[with] digitized Fiat currency.”

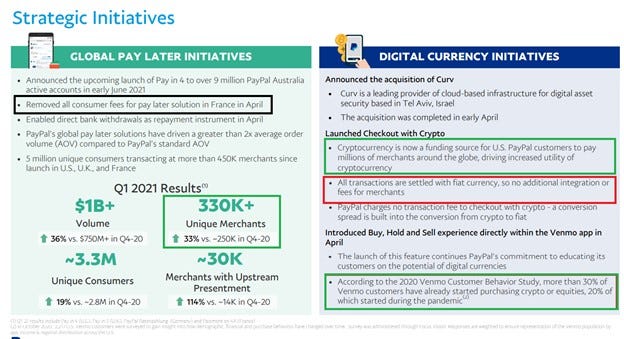

- Acquired Curv, digital asset security provider, in support of its crypto efforts

- Now that U.S. PayPal customers can pay merchants around the globe using crypto, 30% of Venmo customers have already started purchasing crypto or equities

- PayPal continues to invest in adding new merchants to its ecosystem with 31 MM active merchant accounts. 1 MM merchants are now accepting PayPal and Venmo QR codes

- PayPal’s ability to ramp up merchant acquisition has accelerated its Buy Now Pay Later initiatives

Square (SQ): Market Cap: $106.3 Bn, P/E ratio 285.2x, P/S ratio: 7.8x

- Revenue of $5.1 Bn in Q1 2021 (+266% YoY) driven by Bitcoin

- Gross Profit of $964 MM (+79% YoY) driven by Cash App (+171% YoY) and Seller(+32% YoY) ecosystems

- Square continued to drive customer acquisition and engagement with Cash Card, Boost (instant discounts), direct deposit, stock brokerage, bitcoin investing, and business accounts

- Square Financial Services, will expand access to banking services to small businesses

- In March, Cash App inflows increased 55% compared to February, driven primarily by an increase in government disbursements

Square customers were able to access their funds up to two days early and spent their funds on critical needs such as rent, car payments, food and utility bills. All without touching physical money or a credit card. The future of money has arrived…(in the U.S. anyway).

We note most of those functions have been available on Asia social media networks such as WeChat or AliPay since 2014. (Keep an eye out on Facebook’s Diem network coming soon…)

Marqeta is Looking to IPO

Marqeta, led by CEO Jason Gardner, intends to share its IPO plans with the general public on May 14. The fintech firm is currently valued at ~$4.3 Bn, but that is expected to increase 2x to 3x in an IPO. In February, Marqeta confidentially filed its public offering prospectus with the SEC. Goldman Sachs has been confirmed to be leading the firm’s listing with assistance from JPMorgan.

Marqeta provides debit cards and other financial products to large firms such as Square and DoorDash, generating earnings from charging transaction fees and other offerings.

OnDeck Takes Over Enova’s Lending Portfolio

Enova CEO David Fisher declared that the “integration of OnDeck is largely complete.” During the Q1 2021 earnings call, Fisher said that Enova is expected to receive over $200 MM in total cash from the OnDeck portfolio.

Enova reported that small business lending was now more than 50% of their portfolio and has recorded originations of $322 MM in small business funding in Q1. OnDeck’s lending business has also allowed the company to price a $300 million securitization debt facility, backed by OnDeck term loans and lines of credit.

Fintechs that focused on small business loans were hammered during the pandemic last year forcing OnDeck to merge with Enova and Kabbage getting acquired by Amex. We wrote about the challenges impacting small business lenders, including ONDK, presaging the Enova acquisition here as well our take on the Enova bet here.

Matt Harris has announced in a Medium post that Noah Breslow is joining Bain Capital Ventures. Matt, arguably the first fintech VC, was an early backer and board member of OnDeck. We wish Noah well in his new endeavor!

We hope you made money positioning your companies and portfolios appropriately with our in-depth analysis and analytical tools. If you did, you can send some Ethereum to our Ethereum address to 0x1c36906aC1E0353b3680e5Cb466b5Cd60ACA6a01 (kidding, not-kidding :).

In the News:

- Consumer Demand Drove U.S. Imports to Record High in March (WSJ, 5/4/2021) The trade deficit expanded 5.6% to $74.4 Bn as imports were up 6.3% and exports rose 6.6%.

- Congress’s inaction on ILCs, fintech charters worries bankers (American Banker, 5/4/2021) Banks believe that the lack of capital and liquidity requirements for fintechs puts consumers at risk.

- 7 Operations Weak Spots That Hamstring Banks’ Digital Progress (The Financial Brand, 5/7/2021) According to a study conducted by Accenture, operational maturity is advancing slowest among financial institutions compared to all other industries studied.

- Klarna storms ahead of rivals across Europe and US, counting 16m+ new users in 2020 (Sifted, 5/4/2021) According to data from Apptopia, Klarna downloads in the U.S. are more than Affirm and Afterpay combined.

- AWS launches FinSpace analytics service for FS firms (FinExtra, 5/4/2021) Amazon FinSpace reduces the time it takes to find, prepare, and analyze financial data from months to minutes.

- Fintech Unicorn Marqeta Might Conduct IPO as Early as Next Month: Report (Crowdfund Insider, 5/2/2021) Oakland-based payments processor Marqeta, is expected to share its IPO plans to the public on May 14th.

- OnDeck Proving to be Extremely Valuable Acquisition for Enova (Debanked, 4/30/2021) Enova reported that small business lending was now more than 50% of their portfolio and has recorded originations of $322 MM in small business funding in Q1.

- Why did Bill.com pay $2.5B for Divvy? (Techcrunch, 5/6/2021) Bill.com is buying Divvy, the Utah-based corporate spend management startup, for approximately $2.5 Bn.

Lighter Fare:

- Grumpy Dogs Outperform the Friendlies on Some Learning Tests (NY Times, 5/6/2021) Your grumpy dog might have some hidden talents.